-

Rob McKenna and Healthcare

Earlier this week Attorney General Rob McKenna joined a lawsuit filed by a number of other AGs nationally to attack the new healthcare bill adopted in the other Washington. Here’s his press release on the suit: http://www.atg.wa.gov/pressrelease.aspx?&id=25402 He’s using 10th amendment grounds to do so, and my personal read is that the suit is unlikely…

-

Arts bill fails again

-

Interesting Pension Fund Data

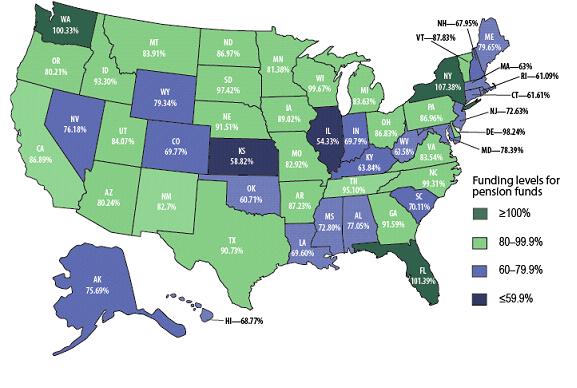

The following was included in the most recent issue of Capitol Ideas, the magazine published by the Council of State Governments: “A new report from the Pew Center on the States finds a $1 trillion gap between the $2.35 trillion states have set aside to pay for employees’ retirement benefits and the $3.35 trillion price…

-

What’s a Tax Loophole?

When you and I sell our homes, we pay real estate excise tax. So how come some businesses don’t pay it on multi-million-dollar transactions? If we hire contractors to remodel our homes, those contractors must charge sales tax on their labor. But some developers have figured out a way to avoid paying that tax on…

-

520 Bridge Moves Forward!

-

Microsoft goes strong on 520

Microsoft has started a huge new campaign to get the legislature to (finally) approve moving forward on the 520 bridge. The Seattle PI covered it here http://blog.seattlepi.com/microsoft/archives/195479.asp Microsoft even has their own website for the campaign, and a full page newspaper ad. I’m starting to get mail from people about it, and I agree. I…

-

Mr. Yuk

-

Using the Gavel

I’ve had a couple of questions about the hearing we held this weekend on the Senate bill to temporarily suspend Initiative 960. I’ll write about the bill elsewhere but I wanted to talk briefly about how difficult it is to manage a large hearing on a contentious issue. This particular hearing was held at 9:00…

-

Eastside residents invited to February 20 town hall with local legislators

CALENDAR ANNOUNCEMENT Eastside residents invited to February 20 town hall with local legislators February 11, 2010 State Sen. Rodney Tom (D-Bellevue) and Reps. Ross Hunter (D-Medina) and Deb Eddy (D-Kirkland) invite Eastside residents to a Town Hall on Saturday, February 20 for a discussion of the current legislative session. The legislators will provide updates on…

-

New Economic Forecast Available

The Washington Economic and Revenue Forecast Council (of which I am a member) released its Washington State Economic Review on Friday. The document is a pretty good read. It comes out a week before our revenue forecast does and experienced tea leaf readers can often predict the revenue forecast from this document. Flat is the…