-

Tax Evasion for Dummies, the video

-

Town Hall Meeting Tonight – Tuesday May 18, 2010

We sent this notice out 2 weeks ago, but I wanted to re-post it today so that you can change all of your plans to come. We intend to have an interchange with constituents on budgets, education, transportation and any other topic that comes up. We’d love to see you. Washington State Legislature Sen. Rodney…

-

What’s candy?

This year the Legislature extended the sales tax to candy. Earlier this week the Dept. of Revenue released a list of products that will be taxed. The list also identifies similar items that don’t fall under the definition of “candy” so that retailers can easily re-program their cash registers. Of course, this provided lots of…

-

WA “Economic Nexus” bill dinged by Tax Foundation

The Tax Foundation, one of my personal favorite conservative tax research organizations, wrote about a new law passed this year by the Legislature. The bill attempts to level the playing field between in-state and out-of-state companies by taxing them the same for business they do inside Washington. The Tax Foundation objects. They’re wrong.

-

Town Hall May 18 – 6pm Bellevue City Hall

Washington State Legislature Sen. Rodney Tom, Rep. Ross Hunter and Rep. Deb Eddy 48th Legislative District CALENDAR ANNOUNCEMENT Eastside residents invited to May 18 town hall with local legislators May 5, 2010 State Sen. Rodney Tom (D-Bellevue) and Reps. Ross Hunter (D-Medina) and Deb Eddy (D-Kirkland) invite Eastside residents to a Town Hall on Tuesday,…

-

America on Display

I spent the better part of the week in DC. I’m Washington’s representative to the “Streamlined Sales and Use Tax Agreement” Governing Board. This is a group of states working to simplify their sales tax systems to make it easier for national businesses to comply with sales taxes in all the states, not just their…

-

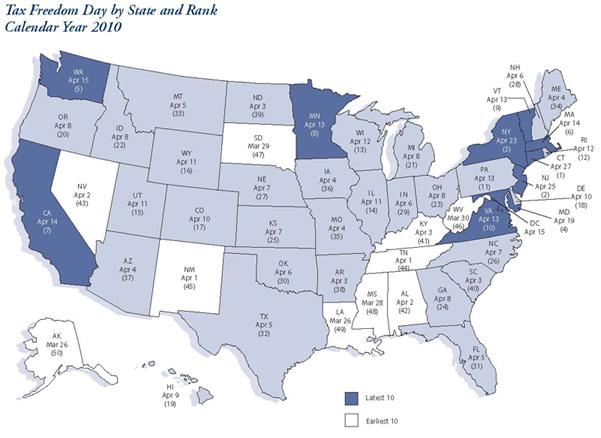

Tax Freedom Day?

One of my favorite thinktanks (The Tax Foundation – www.taxfoundation.org) a conservative tax research organization releases an annual report listing “tax freedom day” for each state. This is the day when you’ve finished paying your combined state, federal, and local taxes for the year. As is usual with soundbite politics the data behind is somewhat…

-

How a New Jobless Era Will Transform America

Last month’s Atlantic Magazine has a great article on the transformative effect the current recession will have on people in America over the next few decades. It’s a little depressing a read, but very thought-provoking. http://www.theatlantic.com/magazine/archive/2010/03/how-a-new-jobless-era-will-transform-america/7919 Here’s the blurb the magazine uses to intro the article: The Great Recession may be over, but this era…

-

Arts bill fails again

-

What’s a Tax Loophole?

When you and I sell our homes, we pay real estate excise tax. So how come some businesses don’t pay it on multi-million-dollar transactions? If we hire contractors to remodel our homes, those contractors must charge sales tax on their labor. But some developers have figured out a way to avoid paying that tax on…