I don’t comment much on the “other Washington” but I have to say that I’m a little frustrated at the game of “chicken” we’re seeing played, and the impact we expect it to have here in “our Washington.” The foodfight they had about the debt limit had drastic impacts on consumer and investor confidence, and that will have impacts on the economy here at home.

I don’t comment much on the “other Washington” but I have to say that I’m a little frustrated at the game of “chicken” we’re seeing played, and the impact we expect it to have here in “our Washington.” The foodfight they had about the debt limit had drastic impacts on consumer and investor confidence, and that will have impacts on the economy here at home.

The Economic and Revenue Forecast Council (ERFC) will release its quarterly forecast of expected revenue for the state next week on the the 15th. I don’t expect it to be pretty, with a decline in the $1 to $2 billion range. Since our last forecast in June the national economy has significantly worsened and we are expecting a large decline in our revenue forecast. The ERFC has a series of meetings and presentations leading up to the official release of the forecast. Last week’s was the initial economic review, where the forecaster (Dr. Raha) sets out his assumptions about the economy and the council approves them. We had a spirited discussion of the accuracy of our normal data streams about construction activity and national GDP estimates, but in the end decided to stay with the current methodology, even though it has been wrong in the same direction 13 quarters in a row, and soon to be 14.

The presentation used at the meeting was the “September Economic Review Notebook.” Here’s the top-line summary:

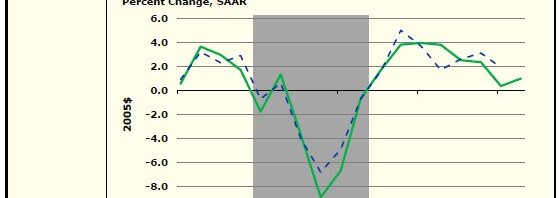

Events since the last forecast in June have turned us increasingly pessimistic about the outlook for the future. It has become clear that global growth is slowing sharply. Revisions to U.S. real Gross Domestic Product (GDP) by the Bureau of Economic Analysis (BEA) show a much deeper recession than previously estimated, and a U.S. economy close to stall speed in the first half of this year. The probability that this fragile recovery gives way to another recession has increased, though it is still premature to say with certainty whether or not it will. Europe’s economy too is on the verge of recession as its sovereign debt problems appear to be spreading. In many ways its troubles are more intractable than those of the U.S., and will likely be a drag on global growth for quite some time. China and India continue to grow, albeit at a slower rate than before. However, two relevant points need to be made here: first, these economies are not yet big enough to drive global growth without any help from the economies of the U.S., Europe or Japan; secondly both these economies are experiencing wage-push inflationary pressures, which are likely to further slow their growth. Washington’s economy is not immune to this slowdown in the global economy, and in fact is closely tied to global conditions due to our export intensity. So our outlook for economic activity in the state has weakened as well.

The rest of the document is worth reading. You can watch the presentation on video, through the miracle of video streaming. Most economists I’ve talked to expect that the negative revisions in the national economic picture are likely to result in a downward adjustment of our revenue projections for the current biennium of somewhere between $1 and $2 billion, in addition to the half-billion we lost in the June forecast. We are currently about $115 million negative, not counting the rainy day fund, or about $150 million positive with it.

As you can imagine, none of us are excited about this, and about the impact on our budget. The Governor asked her staff to come up with both 5% and 10% reduction scenarios in their budget planning exercise, and both our staff and Senate staff are working on a similar project.

We won’t know the size of the problem exactly until the 15th, but the consensus of most analysts is pretty consistent about the direction and magnitude of the decline we will see. At this point we have not made any decisions about where we should go and are looking at a lot of meetings over the next few weeks and months to figure it out, but we are not overly endowed with time to resolve the problem.